Trusted Insurance Solutions in Santa Cruz County – Protecting Your Business, Farm & Family

Living and working in Santa Cruz County offers incredible opportunities—but it also comes with unique risks. From coastal weather exposures to agricultural operations and growing local businesses, having the right insurance coverage is essential. At Scurich Insurance Services, we help individuals, families, and business owners in Watsonville and surrounding communities protect what matters most.

Living and working in Santa Cruz County offers incredible opportunities—but it also comes with unique risks. From coastal weather exposures to agricultural operations and growing local businesses, having the right insurance coverage is essential. At Scurich Insurance Services, we help individuals, families, and business owners in Watsonville and surrounding communities protect what matters most.

With access to over 50 top-rated insurance carriers, we provide customized coverage solutions designed to fit your specific needs—not a one-size-fits-all policy.

Comprehensive Insurance Solutions for Santa Cruz County

Whether you’re running a business, managing a farm, or protecting your home and family, Scurich Insurance Services offers a full range of coverage options:

- Commercial Insurance Packages – Tailored policies that combine general liability, property, and other essential protections

- Farm & Agricultural Insurance – Specialized farm packages with potential Farm Bureau discounts

- Workers’ Compensation – Protect your employees and stay compliant with California regulations

- Professional Liability – Coverage for service-based businesses facing errors & omissions risks

- Umbrella Insurance – Additional liability protection beyond standard policy limits

- Group Benefits – Group health, life, and employee benefits to attract and retain talent

- Personal Insurance – Auto, home, life, and health coverage for individuals and families

Local Expertise That Makes a Difference

Insurance isn’t just about policies—it’s about understanding risk. Our team works closely with you to evaluate your exposures and build a smart risk management strategy. Whether you’re a small business owner, a contractor, or part of Santa Cruz County’s agricultural community, we bring local knowledge and industry insight to every recommendation.

We understand the challenges faced by businesses in Watsonville, Aptos, Santa Cruz, and surrounding areas—from liability concerns to employee coverage and long-term planning.

Why Choose Scurich Insurance Services?

- Access to 50+ insurance carriers for competitive options

- Customized coverage strategies based on your unique needs

- Local expertise in Santa Cruz County industries

- Risk management guidance beyond just selling policies

- Responsive, relationship-driven service

Protect What You’ve Built

Your business, your farm, your home – these aren’t just assets. They represent years of hard work and dedication. Having the right insurance coverage ensures you’re prepared for the unexpected while positioning yourself for long-term success.

At Scurich Insurance Services, we don’t just provide insurance—we help you plan wisely, reduce risk, and move forward with confidence.

Serving Watsonville & All of Santa Cruz County

We proudly serve clients throughout Watsonville and the greater Santa Cruz County area. Whether you’re reviewing your current policies or starting fresh, our team is ready to help you find the right protection at the right price.

Contact Scurich Insurance Services today to review your coverage and discover better options tailored to your needs.

Frequently Asked Questions

What types of insurance does Scurich Insurance Services offer?We offer a full range of insurance solutions including commercial packages, farm insurance, workers’ compensation, professional liability, umbrella coverage, group benefits, and personal insurance such as auto, home, life, and health.

Do you serve businesses in Watsonville and nearby areas?Yes. We proudly serve Watsonville, Santa Cruz, Aptos, and surrounding communities throughout Santa Cruz County with tailored insurance solutions and risk management support.

Can you help with farm and agricultural insurance?Absolutely. We specialize in farm insurance packages and can help identify Farm Bureau discount opportunities, liability protection, property coverage, and workers’ compensation for agricultural operations.

Why should I work with an independent insurance agency?As an independent agency, we represent over 50 insurance carriers. This allows us to compare options and customize coverage that best fits your needs, rather than offering a single carrier solution.

Do you provide risk management guidance?Yes. Beyond insurance policies, we help clients evaluate risks, plan strategically, and make informed decisions to better protect their business, farm, and personal assets.

Looking for better protection? Let Scurich Insurance Services help you build a smarter insurance strategy today.

Read more

What Central Coast Businesses and Homeowners Need to Know

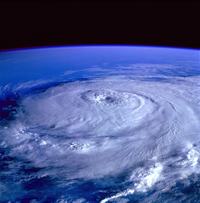

The Central Coast has seen its share of intense weather in recent years — from heavy winter storms and localized flooding to coastal surge events and wind damage. Communities in Aptos, Santa Cruz, Monterey, and Salinas continue to feel the impact of shifting weather patterns that bring stronger storms and longer recovery periods.

Coast has seen its share of intense weather in recent years — from heavy winter storms and localized flooding to coastal surge events and wind damage. Communities in Aptos, Santa Cruz, Monterey, and Salinas continue to feel the impact of shifting weather patterns that bring stronger storms and longer recovery periods.

For homeowners, landlords, contractors, agricultural operations, and business owners, now is the time to review insurance coverage and ensure you’re protected before the next storm hits.

At Scurich Insurance Services in Aptos, CA, we work with families and businesses throughout Santa Cruz County and Monterey County to help them prepare for real-world risks — not just theoretical ones.

Why Storm & Flood Risk Is Increasing on the Central Coast

Recent weather patterns have brought:

-

Heavier-than-normal rainfall totals

-

Flooded roadways and low-lying neighborhoods

-

Mudslides and erosion near burn scar areas

-

Wind damage to homes and commercial properties

-

Agricultural field saturation in the Salinas Valley

Coastal communities like Aptos and Santa Cruz are particularly vulnerable to:

Meanwhile, areas in Monterey and Salinas often face:

Even properties that have “never flooded before” have experienced water intrusion in recent seasons.

Does Your Homeowners Insurance Cover Flooding?

This is one of the biggest misconceptions we see.

Standard homeowners insurance does NOT cover flood damage.

Flood insurance typically requires a separate policy. This applies whether you live:

-

Near the coast in Aptos or Santa Cruz

-

Near the Salinas River

-

In lower-elevation areas of Monterey

-

In inland agricultural zones

If water enters your home from rising ground water, storm runoff, or overflowing creeks — that is generally considered flood damage.

Without a flood policy, repairs can come entirely out of pocket.

What Homeowners Should Review Right Now

If you own a home in Santa Cruz or Monterey County, review:

1. Dwelling Coverage Limits

Are your rebuild limits updated for today’s construction costs?

2. Sewer & Drain Backup Coverage

Storm systems can overwhelm municipal infrastructure. This endorsement can be critical.

3. Flood Insurance Options

Even moderate-risk zones may benefit from coverage.

4. Deductibles

Some policies have percentage deductibles for wind or named storms.

5. Landscaping & Outbuildings

Retaining walls, detached garages, fencing, and outdoor structures may have limited coverage.

Business Owners: Storm Risk Is More Than Just Property Damage

If you operate a business in Aptos, Santa Cruz, Monterey, or Salinas, storms can disrupt:

Important Coverage Areas to Review:

Commercial Property Insurance

Protects buildings, improvements, and contents.

Business Interruption Insurance

Helps replace lost income if you must temporarily close.

Equipment Breakdown Coverage

Covers electrical systems damaged by power surges or outages.

Flood Insurance for Commercial Property

Separate from standard commercial property policies.

Agricultural & Winery Considerations in Monterey & Salinas

The Salinas Valley is one of the most productive agricultural regions in the country. Excessive rain, wind, and flooding can impact:

-

Crops

-

Irrigation systems

-

Equipment

-

Storage facilities

-

Access roads

Specialized agricultural coverage and crop insurance programs may be necessary to properly protect operations.

Coastal Property Risks in Aptos & Santa Cruz

Properties near the ocean face additional exposure to:

-

Salt air corrosion

-

Elevated wind exposure

-

Coastal erosion

-

Wave surge

Insurance carriers evaluate proximity to the coastline carefully. Premiums and deductibles may vary significantly based on location.

Working with a local agency that understands Central Coast geography can make a real difference in proper policy placement.

Why Local Experience Matters

Insurance isn’t one-size-fits-all — especially in areas with unique weather and geographic conditions like Santa Cruz and Monterey counties.

A local agency understands:

-

Neighborhood-specific flood patterns

-

Coastal wind zones

-

Agricultural exposures

-

Construction cost trends in the region

-

Carrier appetite changes after major storm seasons

At Scurich Insurance Services in Aptos, CA, we take a proactive approach — reviewing policies before problems arise.

Storm Preparedness Checklist

Before the next major weather event:

-

✔ Review your insurance policies

-

✔ Confirm flood coverage (if needed)

-

✔ Document property with photos

-

✔ Clear drainage systems and gutters

-

✔ Secure outdoor furniture and equipment

-

✔ Create a business continuity plan

Preparedness reduces both physical damage and financial stress.

Protect Your Property Before the Next Storm

Storm seasons on the Central Coast have become less predictable. Waiting until a major system is forecasted is often too late — especially for flood coverage, which may have waiting periods before activation.

If you live or operate a business in:

-

Aptos

-

Santa Cruz

-

Monterey

-

Salinas

-

Watsonville

-

Capitola

-

Carmel

Now is the right time for a coverage review.

Contact Scurich Insurance Services – Aptos, CA

Whether you’re protecting your home, business, rental property, or agricultural operation, our team can help you evaluate options and identify coverage gaps.

Insurance is about preparation — and preparation starts before the storm clouds gather.

Read more

Heavy rains, floods, hurricanes can all threaten your home and family this spring. While no amount of preparation prevents volatile spring weather, a home emergency kit helps you prepare to be safe and survive.

Heavy rains, floods, hurricanes can all threaten your home and family this spring. While no amount of preparation prevents volatile spring weather, a home emergency kit helps you prepare to be safe and survive.

Survival Essentials

A warm blanket, spare set of clothes and matches could make the difference in your survival. Pack these and all other essential supplies you might need in an airtight container that’s easily accessible.

Food and Water

The Red Cross suggests families store two weeks’ worth of food and water, which means you’ll need one gallon of water per person per day and a variety of easily prepared, non-perishable foods. Don’t forget to stock baby and pet food if necessary, too.

First Aid

Minor bumps and bruises can occur as your family rushes to safety. Your first aid kit should include basic first aid supplies like bandages, antibacterial cream, burn cream and pain reliever. Pack prescription medications, hearing aid batteries and other specialized medications if needed.

Hygiene Items

Toilet paper, toothbrushes and diapers are essential. Hand sanitizer and bleach should also be included in your emergency kit.

Stay Connected

You’ll want to stay connected to the outside world and signal for help, so include a battery-powered radio, extra batteries, your cell phone and chargers in your emergency kit. A flashlight and whistle for each person is also a good idea.

Tools

Whether you have to dig out of the basement or open a soup can, tools come in handy. Stock a multipurpose tool, work gloves, scissors, shovel, screwdriver set, hammer and manual can opener in your kit.

Important Papers

In the rush of an evacuation, you may forget to grab your purse or wallet. Copy important papers like your driver’s license, birth certificate, insurance policies and medical information. Store them, extra cash and your family’s emergency contact information in a waterproof bag to keep them safe.

This home emergency kit will play a big role in keeping you safe when volatile spring weather strikes. Update your insurance policies, too, as you stay protected and prepared.

Read more

National Cybersecurity Awareness Month (NCSAM) occurs annually in October. Started in 2003 by the U.S. Department of Homeland Security and private sector sponsors and nonprofit collaborators that form the National Cyber Security Alliance, this annual event promotes cybersecurity and recommends resources for online safety.  You, your family and/or your company can make several preparations this month.

You, your family and/or your company can make several preparations this month.

Host an Educational Event

Begin planning an open house, expo, lecture, or other educational event that focuses on cybersecurity. Depending on your company, you may decide to focus your educational efforts on information that will benefit senior citizens, college students or families. For example, your IT specialist could present advice that helps consumers avoid cybercrime, or you could show customers how to implement security protocols on their electronic devices. Get creative as you prepare to raise cybersecurity awareness during an educational event.

Train Employees

Cybersecurity training should occur year-round, but your employees may be especially receptive to security tips during a month that’s focused on raising awareness. Take advantage of this annual opportunity to discuss topics like choosing secure passwords, securing electronic devices used for work and managing email safety. Or choose a different topic based on your unique needs.

Focus on Different Weekly Topics

This year, NCSAM includes four weekly topics. In summary, those topics include:

- Online safety at home.

- Training for a cybersecurity career.

- Ensuring online safety at work.

- Safeguarding critical infrastructure throughout the nation.

Your company can prepare to discuss these weekly topics during your events, through customer newsletters and on social media.

Utilize Your Social Media Influence

If your company has a large social media following, you have a powerful platform to raise awareness for cybersecurity. You can write blog posts that outline the importance of cybersecurity, share information about how to join the cybersecurity workforce or detail the ways your business protects data. Also, prepare infographs and other visual aids that discuss online safety tips.

Partner with Other Companies

Like NCSAM was started through a collaboration, your company can partner with other businesses as you increase cybersecurity awareness. Share the latest cybersecurity information, create resources that educate the public about cybersecurity or host an online safety seminar together.

Check your Cybersecurity Insurance Coverage

Cybersecurity insurance protects your business in many circumstances. Review your needs with your insurance agent as you ensure you have the correct amount of cybersecurity insurance for you and your company.

As your business prepares to celebrate National Cybersecurity Awareness Month in October, consider taking these steps now. They give you the tools you need to raise cybersecurity awareness among your employees, customers and community.

Read more

With the Olympics in it’s third week and summer in full swing here, it’s a good time to talk about insurance coverage for water sports businesses – specifically works compensation. Owning a water sport business can be fun and a good investment, but you need to hire employees to help the business run smoothly. Be sure you purchase adequate Workers’ Compensation to cover your employees and protect your assets.

With the Olympics in it’s third week and summer in full swing here, it’s a good time to talk about insurance coverage for water sports businesses – specifically works compensation. Owning a water sport business can be fun and a good investment, but you need to hire employees to help the business run smoothly. Be sure you purchase adequate Workers’ Compensation to cover your employees and protect your assets.

Covered Water Sport Businesses

Your water sports business could encompass dozens of activities in, on or near water. Whether you offer one or several sports, you will need Workers’ Compensation for your business. Example of water sports offerings include:

- Fishing

- Boating, Sailing, Yachting

- Kayaking, Tubing, Canoeing

- White Water Rafting

- Jet or Water Skiing

- Parasailing

- Kneeboarding, Skimboarding

- Kitesurfing, Kiteboarding

- Hoverboarding, Flyboarding, Wakeboarding

- Paddleboarding, Paddle Surfing

- Snorkeling or Scuba Diving

- Swimming and Diving

- Polo

- Surfing

What is Workers’ Compensation?

Many states require business owners to purchase Workers’ Compensation for employees, including seasonal and temporary workers. It pays certain expenses employees incur if they are injured or suffer an illness while performing work-related tasks.

Workers’ Compensation benefits can pay for:

- Medical care

- Lost wages

- Death benefits

- Vocational rehabilitation

Every Workers’ Compensation insurance policy has two parts.

Part One or Coverage A addresses your statutory liability, meaning the coverage your state requires you to carry. It includes no coverage limits and will pay all claims regardless of any benefit changes your state makes.

Part Two addresses employer liability for any employees that are exempt from Worker’s Compensation coverage. These employees could include independent contractors like boat owners or dive instructors who do not purchase their own Worker’s Compensation policy. Part Two can also cover legal expenses from third-party lawsuits.

Why you Need Workers’ Compensation for Your Water Sport Business

Whether your business operates year-round or seasonally, you value your employees and want to protect them from injuries or illnesses. However, accidents happen. You will want to provide financial resources that help your employees navigate their recovery and return to full health and work as quickly as possible.

Adequate Workers’ Compensation protects your business, too. It can protect your assets if you are sued by an employee, and it can pay legal expenses related to any lawsuits. Workers’ Compensation coverage also protects you from fines levied by your state if you don’t purchase adequate coverage.

Contact Your Insurance Agent

For more information on Workers’ Compensation for your specific water sport businesses, contact your insurance agent. He or she will assist you in understanding and complying with your state’s Workers’ Compensation laws. Your agent will also help you purchase the policy that’s right for your business and needs.

With the right Workers’ Compensation policy, you receive peace of mind. It protects your employees and your assets as you help your customers have fun while playing on the water.

Read more

In legal terms, an act of God isn’t, in fact, a religious experience. Well, that’s not to say that an act of God couldn’t be a religious experience, it’s just that that’s not inherent in the legal definition of the term. An act of God essentially comes down to the unforeseen and the unpreventable. You can reduce the likelihood of accidents on the job site by making sure that you don’t allow any drinking, fighting or general carelessness on site, you can reduce the likelihood of accidents on the road through proper auto maintenance, but you can’t prevent a flood or an earthquake no matter how many safety courses you attend.

In legal terms, an act of God isn’t, in fact, a religious experience. Well, that’s not to say that an act of God couldn’t be a religious experience, it’s just that that’s not inherent in the legal definition of the term. An act of God essentially comes down to the unforeseen and the unpreventable. You can reduce the likelihood of accidents on the job site by making sure that you don’t allow any drinking, fighting or general carelessness on site, you can reduce the likelihood of accidents on the road through proper auto maintenance, but you can’t prevent a flood or an earthquake no matter how many safety courses you attend.

Acts of God will exempt a party from strict liability and from negligence in common law. Many building contracts have a provision allowing for acts of God to excuse unexpected delays in a project’s completion. However, damages and delays owing to a natural disaster may be disputed as acts of God in some circumstance.

The key word is “unforeseeable.” If someone falls off of a scaffolding and spends the next four weeks in a cast because of an earthquake, then that will usually be chalked up to an act of God. If they saw a storm coming in, decided to keep working, and then got struck by lightning, then the “act of God” claim may be contested.

“Act of God” is sort of a liability free-pass card, exempting you from responsibility for things that you couldn’t possibly have predicted. There are a few steps that you can take to ensure that there is no gray area, no room for doubt when you need to lean on this legal term:

- Keep tabs on the weather. Don’t assume, for instance, that a storm “isn’t going to be as bad as they say.” It might not be so bad, but do you want to bet your career on it?

- Keep all of your safety equipment in tip top shape. You don’t want to give people any wiggle room to say that that safety harness would have snapped eventually with or without the earthquake.

- This goes for your vehicles, as well. It’s hard to claim a small flood as an “act of God” when your truck was the only one slipping and sliding across the road.

An act of God can be a godsend when it comes to liability, but things have to line up correctly.

Read more