Business leaders make decidions each day on a range of issues including things like hiring, firing, compensation, promotions and the work environment. Every one of these decisions impacts your employees and, depending on the outcome, could result in a claim related to wrongful employment practices.

These claims can disrupt business, hurt morale, damage your reputation and lead to serious financial damages. Thankfully, employment practicies liability (EPL) insurance can provide organizations with protection from the above risks. Specifically, EPL insurance provides the following to policyholders.

Coverage for alleged acts.

EPL insurance not only protects organization from actual wrongful acts, but alleged acts as well. Specifically, EPL coverage can safeguard an organization from claims related to discrimination, harassment, retaliation and wrongful termination.

Timely responses to lawsuits.

Employees suing their employers is common, and orginzations will want to be prepared. This is especially important when you consider that there is no cap on how much a jury can award and that settlements in employment-related cases can easily reach six-figures.

Access to legal help.

Strong EPL policies provide the insured with access to legal resouces. This can prove invaluable if you need advice quickly.

Risk management strategies.

While employment-related lawsuits can arise at any time, organizations that take the time to implement basic risk controls are better equipped to avoid claims altogether. Many insurance companies provide access to risk management training and human resources consulting. These services can greatly reduce the likelihood that your company is sued by an employee.

Additional protection for your directors and officers.

While directors and officers (D&O) insurance can defend against employment-related lawsuits, dedicated EPL insurance is necessary for many orginzations.Having a policy that provides separate coverage for lawsuits connected to wrongful terminations, discrimination, invasion of privacy and similar employent claims ensures that the limits on your D&O policy aren’t exhuasted unnecessarily.

Read more

When cyber attacks like data breaches and hacks occur, they can result in devastating damage. Businesses have to deal with business disruptions, lost revenue and litigation. It is important to remember that no organization is immune to the impact of cyber crime. As a result, cyber liability insurance has become an essential component to any risk management program.

Cyber liability insurance policies are tailored to meet your company’s specific needs and can offer a number of important benefits, including the following:

Data breach coverage.

In the event of a breach, organizations are required by law to notify affected parties. This can add to overall data breach costs, particularly as they relate to security fixes, identity theft protection for those impacted by the breach and protection from possible legal action. Cyber liability policies include coverage for these exposures, thus safeguarding your data from cyber criminals.

Business interruption loss reimbursement.

A cyber attack can lead to an IT failure that disrupts business operations, costing your organization both time and money. Cyber liability policies may cover your loss of income during these interruptions. What’s more, increased costs to your business operations in the aftermath of a cyber attack may also be covered.

Cyber extortion defense.

Ransomware and similar malicious software are designed to steal and withhold key data from organization until a steep fee is paid. As these types of attacks increase in frequency and severity, it’s critical that organizations seek cyber liability insurance, which can help recoup loses related to cyber extortion.

Forensic support.

Following a cyber attack, your organization will have to investigate to determine the extent of the breach and what led to it. The right policy can reimburse the insured for costs related to forensics and seeking out expert advice. Additionally, some policies can provide 24/7 support from cyber specialists, which is especially useful following a hack or data breach.

Legal support.

In the wake of a cyber incident, businesses often seek legal assistance. This assistance can be costly, Cyber liability insurance can help businesses afford proper legal work following a cyber attack.

Coverage beyond a general liability policy.

General liability policies don’t always protect organizations from losses related to data breaches. What’s more, data is generally worth far more than physical assets, and it’s important to have the right protection in place when you need it most. Supplementing your insurance with cyber coverage can provide you with peace of mind that, in even of an attack, your organization’s financial and reputational well-being is protected.

To learn more about cyber liability insurance, contact us today.

Read more

Serving alcohol is a common practice for restaurants, bars, catering companies, entertainment venues and similar establishments. While providing a wide array of beverage options is important, serving alcohol in particular can create a variety of risks for business owners.

For instance, if a patron of your business becomes intoxicated and injures a third party or causes property damage, you could be held liable for the damages. In order to protect your business from serious financial and reputational losses, it’s important to consider purchasing liquor liability insurance.

What is Liquor Liability?

The term liquor liability refers to an organization’s legal and financial responsibility for the actions of individuals who consume alcohol at their establishment. Under liquor liability laws, a business can be found liable for both the bodily injury and property damage caused by a person they improperly served alcohol to.

What is Liquor Liability Insurance?

Liquor liability insurance is designed to protect any business that sells or serves alcoholic beverages. Specifically, this type of insurance covers damages that result from things like fights, careless behavior or automobile accidents caused by individuals who have consumed alcohol.

Liquor liability is important, as it protects you should your clients or patrons sue your business for damages related to their intoxication—something a general liability policy won’t cover.

Most businesses carry a general liability policy, which covers claims against your business for bodily injury, property damage or personal injury. While these policies often include host liquor liability coverage, they only provide protection related to the incidental service of alcohol. While host liquor liability may protect you if you are simply serving alcohol at a company party, it does not offer the coverage you need if you sell alcohol as part of your business.

What’s more, the majority of states require establishments that serve, sell or assist in the purchase of alcohol to carry liquor liability insurance. As such, it’s important to know what to look for in a policy.

What Should My Policy Account For?

When it comes to protecting your business from any kind of liability, it’s critical that you account for common risks. In order to secure the right level of coverage, keep in mind the following policy enhancements when shopping for liquor liability insurance:

Assault and battery coverage.

When alcohol is involved, fights are a common risk. However, many liquor liability policies exclude coverage for assault and battery. Therefore, it’s important to ensure you account for this protection when building your policy. It should be noted that assault and battery coverage can also be extended to include specific incidents such as sexual assault, stabbings and shootings.

Defense costs.

Legal fees from liquor-related claims can easily exceed tens of thousands of dollars. Be sure that your policy accounts for defense costs outside of the policy limit. Otherwise, legal expenses could quickly exhaust your policy limit, leaving little to no insurance to pay for any damages.

Employees included.

Even if you forbid your employees to drink on the job, there’s a chance that they may disregard your instruction. Look for a policy that will cover your employees as patrons to better protect your business from liquor-related incidents.

Mental damages.

In the event of a lawsuit, claimants may allege they were injured in nonphysical ways. In these instances, patrons could sue you for stress, mental anguish or psychological injury. Ensure that your policy accounts for these types of injuries.

It should be noted that liquor liability insurance won’t cover claims that arise from the sale of alcohol to minors or similar illegal transactions. Be sure your employees are instructed to verify patrons are of legal drinking age.

What Determines Pricing?

The underwriting process for liquor liability insurance can differ depending on the type of business you conduct. In general, the following four factors determine the rating and pricing of coverage:

Type of venue. When examining a business’s risk, underwriters look to identify the primary purpose of a venue. If you own a restaurant, the primary purpose of your venue is to serve food, so you are generally considered to have less risk than a nightclub or tavern.

Location of the venue.

Liquor laws can vary drastically depending on the jurisdiction. Each state has its own scoring system based on the nature of local dram shop laws. Dram shop laws impose certain liability standards on area venues that serve alcohol. Because the strictness of these laws may change from location to location, where you operate your business can have a major impact on how your liquor liability insurance is priced.

Percentage of liquor sales.

As a general rule, the more alcohol sales you make, the higher your premiums will be. This factor tends to have more of an impact on pricing than venue type, as a restaurant that has a high percentage of alcohol sales may be priced similar to a bar.

Individual traits of the risk. There are a number of miscellaneous variables underwriters will take into consideration when pricing out policies, including the following:

- Types of entertainment offered

- Experience level of management

- Formal loss control measures

- Security measures and procedures for dealing with intoxicated patrons

Serve Your Patrons Responsibly

When serving liquor, the best way to protect your business from potential claims is through proper risk management and liquor liability insurance. These policies can be complex, and it’s important to discuss the nature of your operations with a qualified insurance broker. Contact Scurich Insurance today to learn more.

Read more

The Occupational Safety and Health Administration’s (OSHA) electronic reporting rule requires certain establishments to report information electronically from their OSHA Forms 300, 300A and 301. Under the rule, the first electronic reports were due on July 1, 2017.

However, on Nov. 24, 2017, OSHA issued a new final rule officially delaying the first electronic reporting deadline to Dec. 15, 2017. Affected establishments will need to submit their reports through the Injury Tracking Application (ITA) website by that time or face possible OSHA penalties.

ACTION STEPS

- Affected establishments must create an account on the ITA website and submit information from their 2016 OSHA 300A form by Dec. 15, 2017.

- Other deadlines under the electronic reporting rule remain unaltered. Therefore, affected establishments should begin their preparations to submit information from all 2017 OSHA forms by July 1, 2018.

Affected Establishments

OSHA’s electronic reporting rule affects establishments that:

- Are already required to create and maintain OSHA injury and illness records and have 250 or more employees;

- Have between 20 and 249 employees and belong to a high-risk industry; and

- Receive a specific request from OSHA to create, maintain and submit electronic records, even if they would otherwise be exempt from OSHA recordkeeping requirements.

The electronic reporting rule applies to establishments, not employers. An employer may have several worksites or establishments. In these situations, some establishments may be affected while others are not.

To determine whether an establishment is affected, employers must determine each establishment’s peak employment during the calendar year. During this determination, employers must count every individual that worked at that establishment, regardless of whether he or she worked full-time, part-time, or was a temporary or seasonal worker.

Finally, a firm with more than one establishment may submit establishment-specific data for multiple establishments.

Reporting Requirements

| Submission Deadline |

Number of Employees

(per establishment) |

| 250+ |

20 -249 |

| Dec. 15, 2017 |

Form 300A |

Form 300A |

| July 1, 2018 |

Forms 300A, 300 and 301 |

Form 300A |

| March 2 (2019 and beyond) |

Forms 300A, 300 and 301 |

Form 300A |

The data an employer must submit and the timeline for submitting this information to OSHA depends on the establishment size.

Establishments with 250 or more employees will be required to submit information from their OSHA Forms 300A, 300 and 301. However, in 2017, these establishments will only be required to submit data from their 300A Form. Establishments in high-risk industries with between 20 and 249 employees will be required to submit information only from their OSHA Form 300A.

For the first reporting year, the deadline has been delayed to Dec. 15, 2017. However, the final rule that delayed the first deadline did not alter subsequent deadlines, so reporting deadlines for 2018, 2019 and beyond remain as shown in the table above.

Submitting the Report

The ITA is a secure website that OSHA created specifically for the data required by the electronic reporting rule. The ITA allows employers three options to submit their reports:

- Manual entry;

- Comma-separated value (CSV) file upload; and

- Application programming interface (API) transmission.

The ITA offers affected establishment instructions and sample files and templates to help them complete the submission process.

OSHA-approved State Plans

The final rule required OSHA-approved State Plans to adopt the electronic rule or “substantially identical” requirements within six months of the final rule’s publication date. The final rule was published on May 12, 2016.

This means that OSHA-approved State Plans have the authority to adopt reporting requirements that go above and beyond what is required by the federal rule. For this reason, establishments located in OSHA-approved State Plan jurisdictions should consult with their local OSHA offices to make sure they are satisfying all electronic reporting requirements.

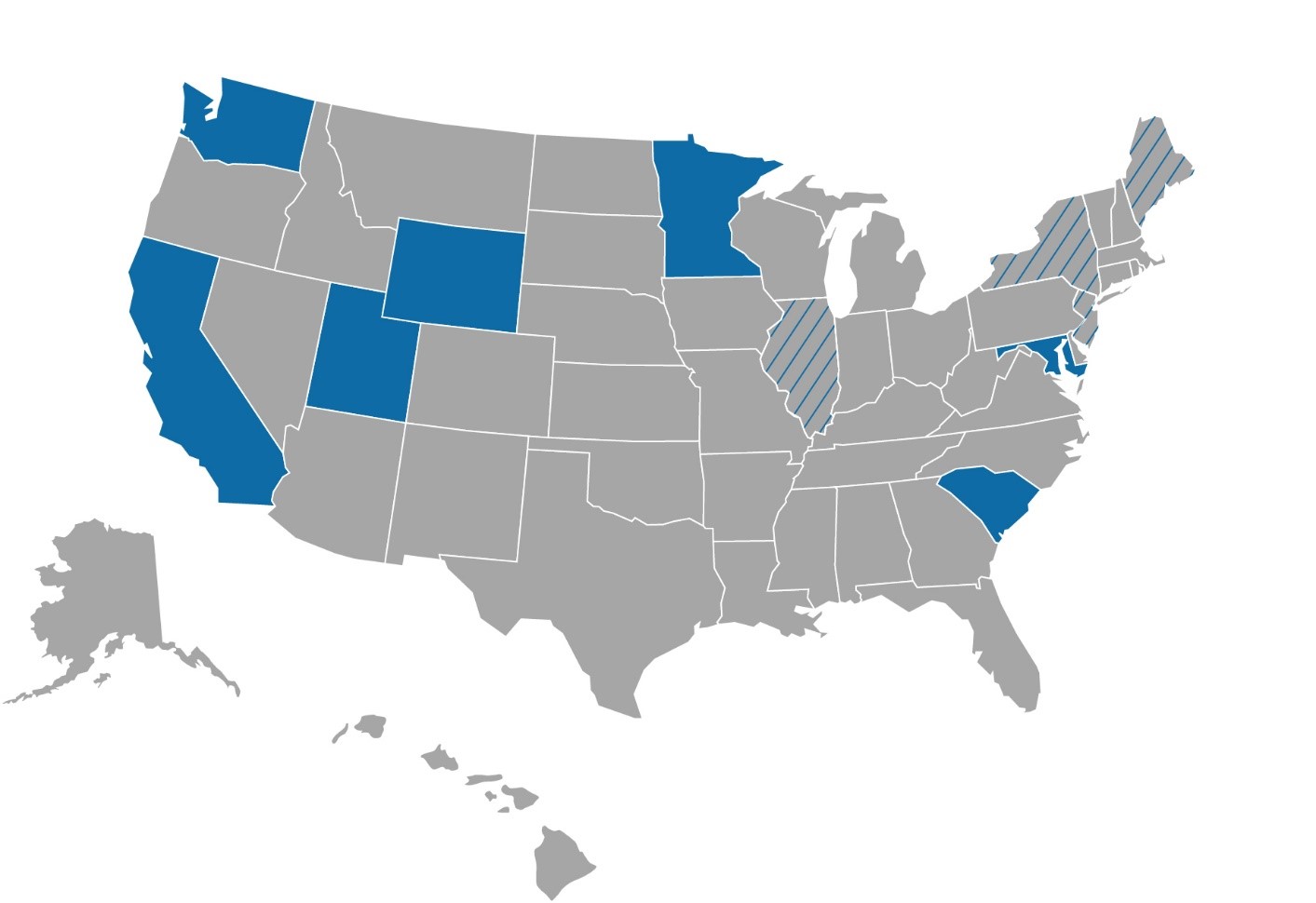

However, the following OSHA-approved State Plans have not yet adopted the requirement to submit injury and illness reports electronically:

|

| All Employers |

Public Employers |

- California

- Maryland

- Minnesota

- South Carolina

- Utah

- Washington

- Wyoming

|

- Illinois

- Maine

- New Jersey

- New York

|

Similarly, state and local government establishments in IL, ME, NJ and NY are not currently required to submit their data through the reporting website.

More Information

Contact Scurich Insurance or visit the OSHA tracking of workplace injuries and illnesses webpage for more information regarding electronic reporting.

Read more

A new law will require California employers with 20 or more employees to grant up to 12 weeks of unpaid, job-protected leave for employees to bond with a new child.

The New Parent Leave Act, enacted on Oct. 12, 2017, extends the state’s parental-bonding leave requirements, which currently apply only to employers with 50 or more employees, to smaller employers starting on Jan. 1, 2018.

The law will allow employees who are employed at a worksite where the employer has 20 or more employees within 75 miles to take parental leave within the first year after their child is born, adopted or placed with them for foster care.

ACTION STEPS

California employers with 20 to 49 employees should become familiar with the new law and revise their leave policies as necessary to ensure compliance.

Employers Subject to the New Law

An employer is subject to the New Parent Leave Act if it:

| ✓ |

Has at least 20 employees working within 75 miles of each other; and |

| ✓ |

Is not subject to the California Family Rights Act (CFRA) and the Family Medical Leave Act (FMLA) |

Thus, the New Parent Leave Act generally applies to all California employers that have between 20 and 49 employees.

Employees Entitled to Leave Under the New Law

Under the New Parent Leave Act, an employee will be eligible to take leave if he or she:

| ✓ |

Has more than 12 months of service for the employer;

|

| ✓ |

Has at least 1,250 hours of service with the employer during the previous 12 months; and |

| ✓ |

Works at a worksite in which the employer has at least 20 employees within 75 miles. |

In addition, an employee that wishes to take leave under the New Parent Leave Act must request and take the leave within the first year after:

| ✓ |

The birth of the employee’s child; |

| ✓ |

The employee’s adoption of a child; or |

| ✓ |

The placement of a child for foster care with the employee. |

An employer may require at least 30 days’ advance notice when the need for leave is foreseeable due to an expected birth or placement of a child for adoption or foster care. If 30 days’ advance notice is not possible, an employee may be required to provide notice as soon as practicable. Employers must respond to an employee’s leave request no later than five business days after receiving it.

Leave Requirements

Before the start of an employee’s leave under the New Parent Leave Act, the employer must provide the employee with a guarantee of employment in the same or a comparable position following the leave. An employer that fails to provide this guarantee may be deemed to have unlawfully refused the employee’s leave request.

Employers are not required to pay an employee while he or she is on leave under the New Parent Leave Act. However, employees may use, and employers may require employees to use, any accrued vacation pay, paid sick time, other accrued paid time off, or other paid or unpaid time off negotiated with the employer, during a period of parental leave.

Like the CFRA and FMLA, the New Parent Leave Act requires employers to maintain and pay for continued group health coverage for an employee while he or she is on parental leave.

The health coverage must be continued at the same level and under the same conditions as those provided prior to a leave period. An employer may recover the costs of maintaining an employee’s health coverage if the employee fails to return to work following a parental leave period for any reason other than a serious health condition or circumstances beyond the employee’s control.

If both parents of a new child are employed by the same employer, the employer is not required to grant more than a total of 12 weeks of leave under the New Parent Leave Act. However, an employer may allow both employees to take up to 12 weeks of leave at the same time.

Prohibited Practices

The New Parent Leave Act prohibits employers from:

| • |

Interfering with, restraining or denying an employee’s rights under the law; and |

| • |

Discharging, fining, suspending, expelling, refusing to hire or discriminating against an employee for exercising his or her rights under the law, or for providing information or testimony in any inquiry or proceeding related to the rights guaranteed under the law. |

Enforcement

If an employer violates the New Parent Leave Act, an affected employee may file a complaint with the California Department of Fair Employment and Housing (DFEH), which may order the employer to:

| • |

Hire, reinstate or upgrade the employee, with or without back pay; |

| • |

Refrain from committing any further violations; and |

| • |

Pay a fine of up to $25,000 for any discrimination. |

The DFEH may also file or grant an employee the right to file a civil lawsuit against an employer for violations of the New Parent Leave Act. Until Jan. 1, 2020, however, employers will have the right to request that all parties participate in mediation before an employee is allowed to file a lawsuit. An employer that receives a right-to-sue notice from the DFEH will have 60 days to submit a mediation request.

Interaction with Existing State Laws

Currently, the CFRA and the FMLA require California employers with 50 or more employees to provide up to 12 weeks of unpaid, job-protected leave for employees to bond with a new child born to, adopted by or placed for foster care with them. The New Parent Leave Act, which was signed into law on Oct. 12, 2017, will require smaller employers in California to provide the same leave.

Unlike the CFRA and the FMLA, however, the New Parent Leave Act will not require employers to provide leave for an employee’s own serious health condition or for the serious health condition of a family member.

Under another existing state law, California employers with five or more employees must grant up to four months of unpaid, job-protected leave to female employees who are disabled by pregnancy, childbirth or a related medical condition. Because of this, an employee cannot take leave under the CFRA for these conditions. Likewise, an employee will not be allowed to take leave for those conditions under the New Parent Leave Act.

However, an employee who works for an employer with 50 or more employees may take CFRA leave to bond with a new child (or to deal with a serious health condition) once her pregnancy disability leave ends. Under the New Parent Leave Act, employees who work for smaller employers will also be allowed to take parental leave after a period of pregnancy- or childbirth-related disability leave.

More Information

Contact Scurich Insurance or visit the DFEH website for more information on California’s leave laws.

Read more

The Problem with Minimum Coverage

Most states require drivers to carry basic liability coverage, which pays for injury and property damages if you are found at fault following an accident. These limits vary by state but can be as low as $10,000 per person or $20,000 per accident.

If you get into an accident, there’s a chance you could be sued. When this happens, minimum liability coverage may not be sufficient to cover the damages, and you could end up paying thousands of dollars out of your own pocket.

What’s more, if you cause an accident and your liability limits are too low to cover the expenses, the other party might go after your assets in court. To protect yourself, it’s important to think critically about how much coverage you need and to secure the proper limits.

How Much Auto Insurance Should I Carry?

While it can be tempting to simply pay the lowest amount possible for auto insurance, doing so can leave you exposed to serious financial risks. In general, it’s recommended that you carry more than the minimum coverage unless you are driving an older car with little value and have no assets to protect.

Did You Know? Insurance is mandatory in order to operate a vehicle in the United States, and every state has specific coverage limits that you must meet. While meeting these minimum limits may be enough to get you on the road, they are often inadequate if you are involved in a serious accident. As such, you may want to consider raising your limits in order to secure the right protection.

The higher you set your coverage limits and the lower you set your deductibles, the less you’ll pay out of pocket after a claim. You will need to determine how much you can comfortably afford when setting your coverage limits and deductibles.

Raising your limits and paying a little more each month will allow you to get the most out of your investment.

Customize Your Policy

When it comes to auto insurance, you have many options. Contact your insurance broker today. They will be able to discuss different ways to customize auto insurance policies, including adjusting collision, comprehensive, medical expenses, uninsured motorist and no-fault coverage. They can also recommend specific policy limits given your situation.

Read more